God’s Body Count Revealed

My Last Word on Capitec’s Brilliant Results

I have spent several decades examining JSE-listed companies and ended up with a deep fascination for one company — Capitec Bank. I can honestly think of no other post-apartheid South African company that has delivered more for shareholders and clients. It is genuinely an exceptional business. Twenty-four years of consistent growth — from what was originally a micro-lender giving out short-term loans, to the institution that now banks more than half of South Africa’s adult population at a 31% return on equity — is no accident. The business model was innovative and genuinely disruptive to the traditional banking sector. (I did not suffer a concussion and no, they are not paying me now.) Nothing I have ever written about the company in the past, nor what follows, was intended to obscure that success.

Firstly, I hold no position in Capitec shares, directly or indirectly. I do not intend to trade in the shares after publication of this article. I have no relationship with any individual or institution wishing to go long or short the share. It is well known that I have previously allowed everything I was taught about risk-control to go out of the window and I lost a great deal of money shorting Capitec — and have disclosed my stupidity openly before and I am happy to admit it publically again. I have also arrogantly been involved in legal proceedings with Capitec where reckless credit was my plea. That verdict was unfortunately not in my favour. (Hey, why don’t you just leave this company alone already?)

The directors of Capitec are completely aware of the contents of my book, Boland Bankers Behaving Badly, and have made no formal attempt to legally dispute any of its contents. Nevertheless, I have decided to cease publication and distribution of the book. Any copies remaining in bookstores will be the last copies available. Given my track record with Capitec, this may be the wisest financial decision I have made in connection with this company.

Given this background — I ask only that the analysis presented here be engaged on its merits. It is my swan-song on this topic. I write so that I can close the chapter on the things that have been keeping me up at night about this company and leave them for the auditors, shareholders and depositors to address. I was equally focal publicly and in the media about Steinhoff, long before everything unraveled, but I never claimed malfeasance for obvious reasons. Nor do I make those claims here, for those same obvious reasons.

What follows is a series of specific, documented concerns about accounting discretion, disclosure quality, and perhaps to a lesser extent, the design of executive remuneration at Capitec. Each item is drawn from public documents. Each is, in isolation, defensible. However, it is the pattern across all of them together that motivated me to go short, to write the book, and now to write this swan-song article.

Capitec’s full year results for the year ended 28 February 2026 will be published on 22 April. The SENS trading statement has already flagged headline earnings per share growth of between 20% and 25%, placing total headline earnings in the range of R16.5 billion to R17.2 billion. To put that in context, Nedbank reported headline earnings of R17.2 billion for 2025, with HEPS growth of only 3% and a return on equity of 15.4%. These two banks are arriving at essentially the same destination by very different roads. What interests me is not merely the destination, but the fuel being burned along the way — and who is paying for it.

Points To Six documented concerns about accounting discretion, disclosure quality, and executive remuneration at Capitec Bank — each drawn from public documents.

Full Year Results

HEPS growth: 20–25%

Balance sheet: R238bn

HEPS growth: 3%

Balance sheet: ~R700bn

- Q1Insurance income: What is the organic growth rate once both one-off structural uplifts are stripped out, and what is the FY2027 run-rate?

- Q2ECL model: Has the SICR behaviour score threshold ever been independently validated by a party with no financial interest in the outcome?

- Q3Write-off policy: What independent validation has been performed on the current score-based write-off determination model?

- Q4AvaFin: What is the standalone CLR trajectory for FY2026, and at what level would management consider the growth rate unsustainable?

- Q5Capital comparability: Can management provide a prior-period CAR restatement adjusted for Basel IV RWA changes and PA Directive 2 of 2025?

- Q6CFO remuneration: The 2025 report shows a R3,000 strike price difference between simultaneously granted share options and SARs. Can this be clarified?

Issue One: Who Is Really Checking the ECL Numbers?

When a bank lends money, it knows that some loans will not be repaid. Accounting rules require it to estimate those future losses and set aside a financial cushion — called a provision — to absorb them. This estimate is called the Expected Credit Loss, or ECL.

The question is: how does it decide how many people will not pay — and who checks that the estimate is honest? Capitec calculates its ECL using a complex statistical model that tracks how loans move between risk categories over time — from performing, to stressed, to defaulted. The inputs to that model include internal credit scores, employment data, and repayment history. This sounds brilliant, until you realise that all of this data is generated and held by Capitec’s own management.

When Capitec adopted the IFRS 9 accounting standard in 2019, it published a transition report and engaged PwC to provide assurance over it. That assurance was limited in a way that is easy to miss. PwC confirmed that the numbers in the report were compiled correctly from the model’s outputs. It did not audit the model itself — its assumptions, its design, or whether its parameters were set appropriately. The underlying methodology had not been independently verified. PwC checked the maths. Nobody checked the recipe.

This connects directly to how Capitec sorts its loans into risk categories. Under IFRS 9, all loans sit in one of three stages. Stage 1 loans are performing normally — small provision required. Stage 2 loans have deteriorated significantly — much larger provision required. The trigger for moving a loan from Stage 1 to Stage 2 is a Significant Increase in Credit Risk, or SICR.It is worth being precise here, because the comparison with other banks is often overstated. No South African bank — not Nedbank, Standard Bank, ABSA, or FNB — publicly discloses the specific numerical threshold at which a loan migrates from Stage 1 to Stage 2. IFRS 9 does not require them to. The standard leaves the definition of “significant” entirely to management judgement. After seven years of implementation, a consistent industry standard has still not emerged.

Where Capitec differs from its peers is not in the absence of a threshold disclosure — it is in the nature of what the threshold is anchored to. The four major banks use probability of default frameworks for their SICR assessment, anchored at least partly to external or standardised measures: credit bureau data, observable default rates, and the universal IFRS 9 backstop that any loan more than 30 days past due must migrate to Stage 2 regardless of the model’s output. Their external auditors test the SICR models against historical arrears data and forward-looking default rates — observable outcomes that provide at least partial independent verification.

Capitec’s pre-arrears SICR trigger — the one that catches deteriorating borrowers before they miss a payment — is anchored primarily to its own proprietary behaviour score. This score is built entirely on internal Capitec data, calibrated internally, and the threshold at which it triggers a Stage 2 migration is set by management and reviewed annually by management. There is no external anchor disclosed. The auditors test whether the model produces outputs consistent with the criteria — but not whether the threshold itself is set at an appropriate level.

Why does this matter? Capitec has millions of unsecured personal loans — many of which are now in the form of credit cards and revolving credit loans. A small movement in where the behaviour score threshold sits can shift a large number of loans between Stage 1 and Stage 2. Stage 2 loans require substantially larger provisions than Stage 1 loans. A marginal threshold adjustment therefore affects the total provision balance, which affects reported profits, which affects the share price, which — as we shall come to shortly — directly determines how much money Capitec’s executives take home. The dial that controls this is held entirely by management. Unlike at the other four major banks, there is no external reference point against which an outside analyst can independently assess whether it is set in the right place.

Issue Two: A Policy That Keeps Moving Into the Dark

To understand the full picture, you need to follow the history of how Capitec has handled the question of when to write off bad loans. It is a story in three Acts, and each chapter ends with less transparency than the one before.

Act One — Before 2018: The Vanishing Act

Under the old accounting standard, IAS 39, Capitec wrote off debt review loans immediately and in full the moment a client entered debt review. Gone from the loan book, done. Simple and transparent.

However — and this is the nuance my book raised — Capitec simultaneously carried an asset on its balance sheet called the “expected recoveries receivable.” This was management’s own estimate of how much would eventually be recovered from those already written-off loans. By 1 March 2018, this receivable stood at R906 million. This was part of the missing R2.5-R3 billion that Viceroy Research were unable to account for when they tried to reconcile the loan book. But the disclosures were there, you just had to follow the asterisks in the footnotes in every second Annual Report. There was never any independent validation of these estimates. Management wrote off the loan with one hand and added back their own estimate of what they thought they would recover with the other. The net effect on the balance sheet was considerably more optimistic than a straight read of the write-off numbers would suggest. This was the big criticism levied on management in Chapter 17 of Boland Bankers Behaving Badly.

Act Two — March 2018: A Very Brief Moment of Transparency

When IFRS 9 forced a full public disclosure of the write-off methodology, Capitec’s transition report stated the policy explicitly for the first time. Under the new approach, only 20% of a debt review loan would be written off immediately. The remaining 80% would stay on the balance sheet for a further 16 months after the last payment before being written off — the point at which Capitec had calculated that less than 5% of recovery value remained. For handed-over loans, 70% was written off immediately and 30% retained for 6 months.

This was the first mechanically transparent write-off policy Capitec had ever published. Any auditor and any analyst, anywhere in the world, could read that rule, apply it to the disclosed loan book, and arrive at an independent estimate. It was crude, but it was verifiable.

Capitec’s own 2019 annual report acknowledged the direct consequence: a build-up of loans on the balance sheet that were more than three months in arrears and would previously have been written off. The gross loan book was now larger, and it would stay larger for longer. The same 2019 report described this as resulting from “the change in write-off policy” — which was, to be fair, an admirably candid acknowledgement that the numbers had changed for accounting reasons —- the change in accounting standards —- not because the loans were actually any better.

Act Three — Within Twelve Months: Back Into the Black Box

The 2019 annual report then disclosed something that has passed without comment in the South African financial press. The 16-month time-based rule —- barely months old —- had already been abandoned and replaced with a new methodology based on behaviour scores and consecutive missed payments. This was described as a “refinement and simplification.” The write-off point was now determined by internal behavioural scores and internally set thresholds that are not publicly disclosed.

The practical consequence is significant. The old 16-month rule was transparent but arguably imprecise. The new methodology may be more precise, but it cannot be replicated by anyone outside Capitec, because the threshold that determines the write-off point is internal and undisclosed. The progression over seven years — from the IAS 39 recoveries receivable, through the briefly disclosed 16-month rule, to the current score-based methodology — represents a consistent movement in one direction: away from external verifiability and toward management discretion.

Whether this progression reflects genuine improvements in credit risk management, or whether it reflects a preference for keeping the methodology in a dark box following the intense scrutiny of the Viceroy period, cannot be established from the public documents. But, that is precisely the point.

Issue Three: The Evergreening Question

The write-off policy history connects to a concern that Viceroy Research raised in 2018 and that has never been definitively resolved.

Evergreening is the practice of issuing a new loan to a borrower who cannot repay their existing one. The new loan settles the old loan. The borrower’s account is suddenly up to date. Their behaviour score may even improve. The bank’s impairment charge stays clean. The loan never visibly defaults. The practice is not unique to Capitec — it has appeared in lending markets from the Irish property boom to South Africa’s African Bank collapse in 2014 — but it is particularly difficult to detect in an unsecured retail lending book where the average loan size has grown significantly above inflation over a decade.

You know that something is a common-practise when it has several names or expressions for the same practice. ‘Evergreening’ is sometimes also called ‘loan rolling or rolling over loans’ — the most commonly used term in South African banking circles, and the one Benguela used in their letter to Capitec and used by Viceroy in their report ‘A Rolling Loan Gathers No Loss.’ Some other clever names are ‘extend and pretend’, ‘kicking the can down the road’, ‘Zombie lending’ and the euphemism and Capitec’s own term for the practice ‘rescheduling.’ I don’t mind which term you use to substitute for ‘evergreening.’

When Capitec’s personal loan book was written about in Boland Bankers Behaving Badly, average loan sizes had increased tenfold in under a decade to over R66k from a R6.5k average. By August 2025, South African loans and advances had reached R93 billion and their average loan size had continued to increase. Capitec’s explanation — that their client base has moved upmarket as higher-income earners joined the bank — is not implausible.

Viceroy was fined R50 million by the FSCA in 2021 for publishing ‘false and misleading statements’ about Capitec. That finding is a matter of record. However, the story did not end there. In 2022, the Financial Services Tribunal set the fine aside, ruling that the FSCA had no jurisdiction over the US-based partnership. In July 2025, the Pretoria High Court overturned that decision, ruling that foreign conduct with a substantial effect on South Africa’s financial markets falls within the FSCA’s reach. The case is back before the Tribunal. Viceroy has, as of today, paid nothing. The matter of whether a R50 million fine can be collected from a Delaware-registered partnership whose partners are overseas nationals remains, to put it diplomatically, unresolved.

More significant than Viceroy, and far less reported, was a letter sent to Capitec ten days before the Viceroy report by Benguela Global Fund Managers — a credible South African asset manager with no short position and no financial incentive to damage the share price. Benguela warned that unless the board end excessive loan rescheduling, Capitec risked following African Bank’s path.

It is my opinion that the structural conditions under which evergreening could occur without detection remain in place today: internally set and undisclosed SICR thresholds that determine when loans migrate to higher-provision stages, a write-off policy that is calibrated against internal scores that no external auditor or analyst can replicate, and a rapidly growing loan book where average loan sizes have outpaced inflation. This does not prove that evergreening is occurring. Only a full independent model audit could answer that question. No such audit has ever been publicly disclosed.

Issue Four: Paying the People Who Set the Dial

Remuneration at South African banks is a complicated topic. But the specific concern here is not about quantum — it is about structure, and what the structure is designed to incentivise.

Gerrie Fourie, Capitec’s CEO until his retirement in July 2025, received total remuneration of R104.8 million for the financial year to February 2025. Of this, R75 million came from Share Appreciation Rights — instruments that pay out the increase in Capitec’s share price between the grant date and the vesting date, with no capital invested by the executive. In a year when Capitec’s share price rose 52%, the remuneration report stated explicitly that this robust share price growth resulted in above-target payments to executives. Capitec’s executives are not just beneficiaries of a rising share price. A rising share price is the primary mechanism by which they are paid. At the time of writing, Capitec trades at a price-to-earnings ratio of 31.3 times, compared to a peer average of 10.6 times and an African banking industry average of 9.4 times. The share price has outperformed its peers by a multiple of three.

Still, Fourie’s R104.8 million compensation is not excessive. If you compare that to Nedbank’s CEO Jason Quinn received R119.7 million in 2024 — despite Nedbank delivering 3% earnings growth compared to Capitec’s 30%. If you wanted to argue that South African banking remuneration is simply excessive across the board, the Nedbank figure makes that case more powerfully than anything at Capitec. That said, Nedbank’s remuneration framework contains two features absent from Capitec’s that are worth noting.

Nedbank caps its short-term incentive payouts. Capitec does not, at least not in any terms that are publicly disclosed. In a year of exceptional performance, there is no disclosed ceiling on annual bonuses at Capitec. Nedbank also uses externally benchmarked client satisfaction metrics in its long-term incentive structure. Capitec uses a Customer Satisfaction score — CSAT — that constitutes 20% of executive LTI vesting and is defined, measured, and reported entirely by Capitec’s own management. One could argue this is like grading your own exam. Capitec executives have a direct financial interest in the CSAT score being high, and the score is entirely within their control to define and measure.

Directors hold instruments that pay out only when the share price rises. The share price rises when reported earnings grow. Reported earnings are higher when the impairment charge is lower. The impairment charge is lower when fewer loans migrate from Stage 1 to Stage 2. The migration from Stage 1 to Stage 2 is controlled by the SICR threshold. The SICR threshold is set by management. Management’s pay depends on the share price. Each link in that chain is individually explicable. Together they describe a system in which every incentive points in the same direction.

Issue Five: Your Savings, Their Loans

Here is a question South Africa’s 25 million Capitec depositors are unlikely to have asked themselves: do you know where your money is being lent?

Capitec funds its loan book primarily through the savings accounts, fixed deposits, and Global One accounts of ordinary South Africans. Those deposits are now being deployed, in growing measure, into an online consumer lending operation called AvaFin — which lends to near-prime and sub-prime borrowers in Poland, Latvia, Spain, Czech Republic, and Mexico.

AvaFin currently only contributes 2% of group earnings, but that number is intended to grow. At its current loan book expansion rate of 48% per year, and assuming Capitec’s domestic South African book continues growing at a conservative 10% annually, AvaFin will represent approximately one fifth of Capitec’s total loan book by around 2030. In less than five years. The depositor who opened a fixed deposit this week in Stellenbosch is, in a meaningful sense, funding a lending operation in Warsaw.

This is not inherently wrong. Banks diversify geographically. The concern is whether South African depositors understand the risk profile they are now exposed to, and whether the disclosures make that risk sufficiently clear.

Capitec’s domestic credit model was built on a very specific South African customer: typically formally employed, with a salary-based debit order, operating within a well-understood South African legal recovery framework, with years of proprietary credit history informing every lending decision. The credit loss ratio on AvaFin’s book is 42.6% — not because AvaFin is badly run, but because short-term online near-prime lending in Eastern Europe and Latin America operates on a completely different economic model to South African personal loans. The yields are higher, the defaults are higher, and the margin sits in between.

The risk, as it grows in absolute terms, is that South African depositors are exposed to the credit environment of markets they have never heard of. The Mexican peso, for instance, experienced significant volatility over the period during which Capitec began scaling its AvaFin investment. The currency has since recovered — at time of writing the peso sits at approximately 17.9 to the dollar, having strengthened almost 16% in 2025. But currency risk exposure of this kind is not what a South African pensioner signing up for a Capitec fixed deposit believes they are taking on.

Capitec holds a capital adequacy ratio of 33% — almost double the regulatory minimum — and at current scale the buffer between AvaFin losses and depositor funds is substantial. But buffers are there precisely for the risks that grow faster than expected. If AvaFin’s credit loss ratio does not improve as the book grows and the model shifts toward longer-term lending, the compound impairment charge will grow rapidly relative to its earnings contribution. South African depositors are entitled to understand that trajectory clearly. The 22 April full year results should disclose AvaFin’s standalone credit loss ratio and loan book position in sufficient detail for them to do so.

Issue Six: What Kind of Institution Is Capitec Actually Becoming?

There is a question that South Africa’s financial press has not yet asked clearly about Capitec, and it is more interesting than any of the accounting concerns raised in this article.

Capitec is no longer primarily a bank. Some analysts argue that Capitec is a platform to sell product. Nothing more, nothing less.

In FY2025, non-interest income accounted for 67% of total income from operations after credit impairments. Insurance contributed 25% of total earnings. Value-added services — airtime, electricity, data, lottery tickets, vehicle licence renewals — and Capitec Connect together contributed 23%. Personal banking, which includes the loan book, contributed 45% — and within that, transaction fees and commission account for a large portion. The loan book itself, the business Capitec was built on and the one that generates all the accounting concerns discussed earlier in this article, is now a minority driver of total income.

This transformation is either the most impressive strategic pivot in South African banking history, or it is one of the most underanalysed regulatory questions in the country. Possibly both for reasons that I won’t have time to explore in this article.

The positive case is compelling. An institution that earns most of its income from insurance premiums, transaction fees, and airtime commissions is structurally more resilient than one that depends primarily on a loan book. If South African consumers hit a severe credit downturn and default rates spike, Capitec’s earnings are now substantially cushioned by income streams that have nothing to do with whether borrowers repay their loans. That is a genuinely valuable hedge that the traditional big four banks do not have to the same degree.

The risk case is equally real, and it is one that regulators should be examining carefully. Capitec is regulated, supervised, and capitalised as a bank. Its depositors are protected under the banking deposit insurance framework. Its capital requirements are set under the Banking Act and calibrated for bank risk. The SARB supervises it as a bank. But a growing and now substantial proportion of its earnings come from activities that are fundamentally not banking. Selling airtime is a telecoms reseller business. Underwriting funeral policies and credit life insurance on 15 million lives is an insurance business. Running an MVNO dependent on a host network is a telecoms infrastructure business. Lending money to sub-prime borrowers in Poland and Latvia at a 42% credit loss ratio is an Eastern European fintech business.

None of these businesses are inherently problematic. But they each carry risk profiles that are entirely different from South African retail banking, and they are all sitting inside an entity regulated and capitalised as a South African bank. A catastrophic mortality event — a pandemic, a disease outbreak — creates a claims exposure against the insurance business that has nothing to do with credit quality and everything to do with whether Capitec’s actuarial models are adequate. A change in commission structures by Cell-C or another provider could reprice the VAS income overnight. The MVNO depends entirely on a host network relationship that Capitec does not own. AvaFin’s losses in Mexico flow directly into the earnings of a South African bank whose depositors were never told they were funding sub-prime consumer lending in Latin America.

The diversification was smart and probably the right long-term move. But the pace of transformation raises a question that belongs in the public domain: does South Africa’s regulatory framework for banking supervision adequately capture the risk profile of an institution that is simultaneously a bank, an insurer, a fintech, a telecoms reseller, and an international online lender? And do the 25 million South Africans who bank with Capitec — and whose deposits ultimately underpin all of it — understand the institution they are dealing with?

The 22 April full year results will almost certainly show continued strong growth. They should also show, with granular clarity, which portion of that growth is structural and recurring, and which portion reflects the one-off step changes of the past eighteen months: the removal of the Sanlam profit-share from November 2024, and the transfer of approximately 550,000 Guardrisk credit life policies to Capitec Life on 1 September 2025. Both of these transactions boosted reported insurance income in ways that will not repeat in 2027. Analysts who read the headline earnings growth rate without stripping these out will be measuring the wrong thing.

Conclusion: Questions Worth Asking

(For Analysts Attending the 22 April Presentation in Person or Online)

Capitec is a genuinely exceptional business and will in all probability continue to be one. The concerns raised is a consistent thread running through seven years of public documents: a credit loss model whose key parameters are set internally and never independently validated; a write-off policy that has moved through three iterations, each less externally verifiable than the last; structural conditions under which deteriorating loans could remain in Stage 1 longer than their economics warrant; an executive remuneration structure in which every incentive points toward higher reported earnings and a higher share price; a self-measured executive metric with no independent verification; and a rapidly growing overseas lending operation funded by South African depositors who are unlikely to know it exists.

There is also a broader strategic question that deserves to be asked plainly. Capitec is no longer primarily a bank. In FY2025, non-interest income accounted for 67% of total earnings. Insurance contributed 25%. Airtime, electricity, and data sales contributed 23%. The loan book — the business this institution was built on, and the one that generates all of the accounting concerns discussed in this article — is now a minority driver of income. This diversification may well be the right long-term strategy. But it means Capitec is now simultaneously a bank, an insurer underwriting 15 million lives, a telecoms reseller capturing 40% of South Africa’s airtime transactions, an MVNO dependent on a host network it does not own, and an international sub-prime online lender. Each of those businesses carries a risk profile that is different from South African retail banking, and all of them sit inside an entity regulated and capitalised as a South African bank. Whether the regulatory framework has kept pace with that transformation is a question for the SARB, not only for analysts. Whether South Africa’s 25 million Capitec depositors understand the institution their savings are funding is a question for Capitec’s board.

For analysts attending the 22 April results presentation, I would suggest the following specific questions for CEO Graham Lee and CFO Grant Hauptfleisch:

Q1: On insurance income: The Sanlam profit-share terminated in November 2024 and the Guardrisk credit life transfer completed on 1 September 2025. Both events boosted reported insurance earnings in FY2026. What is the underlying organic insurance income growth rate once both one-off structural uplifts are stripped out, and what is the expected run-rate for FY2027?

Q2: On the ECL model: The SICR behaviour score threshold that determines Stage 1 to Stage 2 migration is set and reviewed internally by management. Has this SICR threshold ever been independently validated by a party with no interest in the outcome, and if so, when and by whom?

Q3: On the write-off policy: The 16-month TSLP rule disclosed at the IFRS 9 transition was replaced within twelve months by a behaviour score and missed payment methodology. What independent validation has been performed on the current write-off determination model, and what would cause management to conclude that the threshold needs to be moved?

Q4: On AvaFin: At the current 48% annual loan book growth rate, AvaFin will represent approximately one fifth of Capitec’s total loan book by 2030. What is the standalone credit loss ratio trajectory for AvaFin (based on FY2026) and at what CLR level would management consider the growth rate unsustainable?

Q5: On the Basel IV capital comparability: Can management provide a restatement of the prior period capital adequacy ratio on a basis comparable to the current period, adjusting for the Basel IV operational RWA changes and the Prudential Authority Directive 2 of 2025 insurance equity deduction?

Q6: On the CFO remuneration discrepancy: The 2025 remuneration report shows the CFO’s share option grant at a strike price of R5,056.24 and the simultaneously granted SAR at R2,056.24. The policy states both are granted on the same terms. Can this be clarified?

Whether Capitec’s incentive structure, its disclosure practices, and its accelerating transformation into something considerably more complex than a retail bank are producing the right kind of institution for the 25 million South Africans who bank with it — not just for its shareholders — is a question that regulators, analysts, and the financial press are entitled to ask clearly and to have answered in public.

I remain, as ever, stubbornly curious to see how this all unfolds.

*Jaegur Martin is the author of Boland Bankers Behaving Badly: The Other Unofficial Story of Capitec Bank (Hardly Read Press, 2025) – now out of print. He holds no position in Capitec Bank Holdings Limited directly or indirectly and will not do so following publication of this article.

Capitec is still selling gumball’s and popcorn from video stores

An extract from ‘Boland Bankers Behaving Badly’, chapter 28. ‘Blockbuster’s Strategy’ from pages 139-145

In the summer of 2004, executives of a fledgling DVD-by-mail company called Netflix walked into the gleaming headquarters of Blockbuster Entertainment. They proposed that Blockbuster purchase Netflix for $50 million. The Blockbuster executives—titans of an empire spanning 9,000 stores across the globe—barely suppressed their laughter. Here was this upstart with his ridiculous red envelopes, suggesting he could replace the Friday night ritual of wandering the aisles of America’s favourite video store. They showed the Netflix execs the door. Today, Netflix is worth $386 billion. Blockbuster is a punchline.

Picture millions of South Africans, armed with what were once gold and are now black bank cards, standing patiently in the scorching African sun outside Capitec branches. ATMs from other banks sit empty and ignored just meters away. These customers have found their tribe. They’ve discovered something precious in a country where financial inclusion was a pipe dream: a bank that doesn’t make them feel poor for being poor.

Capitec claims 24.1 million clients in a country of 63 million people, of which only 7.4 million are taxpayers and 29 million are social grant recipients—four for every taxpayer. The official unemployment rate in South Africa is 32.9%, which means that most holders of Capitec bank cards are probably social grant recipients or people that we would technically call “unemployed.”

“What is interesting is when you look at the unemployment rate,” said Fourie in June 2025,” Stats SA doesn’t count self-employed people. I think that’s an area we need to correct. The unemployment rate is probably actually 10%. Just go look at the number of people in the township informal market, who are selling all sorts of stuff, who have a turnover of R1,000 a day.”

They’ve built this empire on radical simplicity: straightforward products, transparent pricing, and lower overall costs. The average Capitec Bank client pays just R48 a month in fees, compared to the Big Four’s average of R247. But here’s where the story takes a curious turn.

While their competitors have been quietly shuttering branches and pulling ATMs from street corners—embracing the digital future that seems as inevitable as sunrise—Capitec has been doing something almost incomprehensible. They’ve been building more branches and installing more ATMs. Many more.

By 2024, Capitec operated 42% more branches than any of the Big Four banks. While the industry’s ATM count plummeted 13% between 2019 and 2024, Capitec increased its count by a staggering 67%. They now run 75% more ATMs than FNB, South Africa’s largest bank. It’s the banking equivalent of opening more video stores in 2005. A poor strategy that’s well-executed doesn’t make it a good strategy; it makes it a well-executed poor strategy.

Fourie defends this counterintuitive strategy with arguments that would sound eerily familiar. Physical branches build trust, he insists. They foster personal connections. South Africans still need cash, still value face-to-face service. The branches and ATMs aren’t just convenient—they’re lifelines.

It’s the same logic that kept Blockbuster executives convinced that customers would always want to browse physical shelves, that the ritual of Friday night movie selection was irreplaceable, and that their stores offered something Netflix’s red envelopes could never match. They weren’t entirely wrong—until they were completely wrong.

Peel back Capitec’s populist veneer, and you discover this isn’t a bank at all, at least not in the traditional sense. Like Blockbuster, which made its real money not from movie rentals but from late fees and concession sales, like popcorn, Capitec’s profits come from somewhere else entirely. Insurance sales. Cellphone top-ups. Electricity payments. The banking is almost beside the point.

Consider the mathematics of their operation. If Capitec truly has 25 million clients, but 11 million are “not fully banked”—generating only minimum fees—that’s roughly R1 billion in monthly revenue from customers who almost certainly cost more to serve than they contribute. It’s a loss-leader strategy that works brilliantly until it doesn’t. Considering the number of active bank accounts claimed by all banks, the total exceeds 86 million. In a population of 63 million, this means that people operate more than one “primary” bank account.

The rest of the chapter can be found here.

Note: The original book includes footnotes and references. To read the rest of the chapter, subscribe to my Substack.

Capitec selected Accounting Standard’s buffet-style

An extract from ‘Boland Bankers Behaving Badly’

Capitec’s Financial Director, André du Plessis, wasn’t one to miss an opportunity to showcase his financial wizardry. Rising impairments—the money a bank sets aside for irrecoverable loans—threatened to spoil the party. But Du Plessis wasn’t about to let pesky details like that place a cap on the rising share price and his bonus. Executive incentives, particularly the long-term Share Appreciation Rewards, were closely tied to an upward trajectory in the share price. In my opinion, when directors care more about the share price than the actual business, it’s like a chef caring more about plating than the taste of the meal. I’ve heard Gerrie Fourie exclaim numerous times that they are not concerned about the share price, but I view this as mere rhetoric. If you aren’t worried about the share price, then why are you incentivised by it going higher?

Numbers can bend the truth without necessarily breaking it. Accounting standards exist to prevent outright cheating, but they also leave room for some artful interpretations, like a jazz musician riffing on a familiar tune. When new rules are introduced, the most skilled players learn to play by them in ways that make them appear like virtuosos.

Banking is a business of perceptions, and a bank’s loan book—the sum of all the money it has lent out — acts as a report card. Investors and analysts pore over it to determine whether the bank is thriving or struggling. So, when accounting standards for loans and recoveries started to shift, Capitec’s leadership spotted a golden opportunity hidden in the so-called “grey zone”. It was an opportunity to dress up the numbers without technically crossing any lines.

At this point, Mouton and PSG Group were firmly back in the Capitec fold, and Markus Jooste still sat on PSG’s board. Did Jooste have anything to do with the accounting gymnastics? Who’s to say? But in hindsight, it’s hard not to admire the sheer audacity of the scheme — a bit like watching someone successfully pull off a disappearing act in broad daylight.

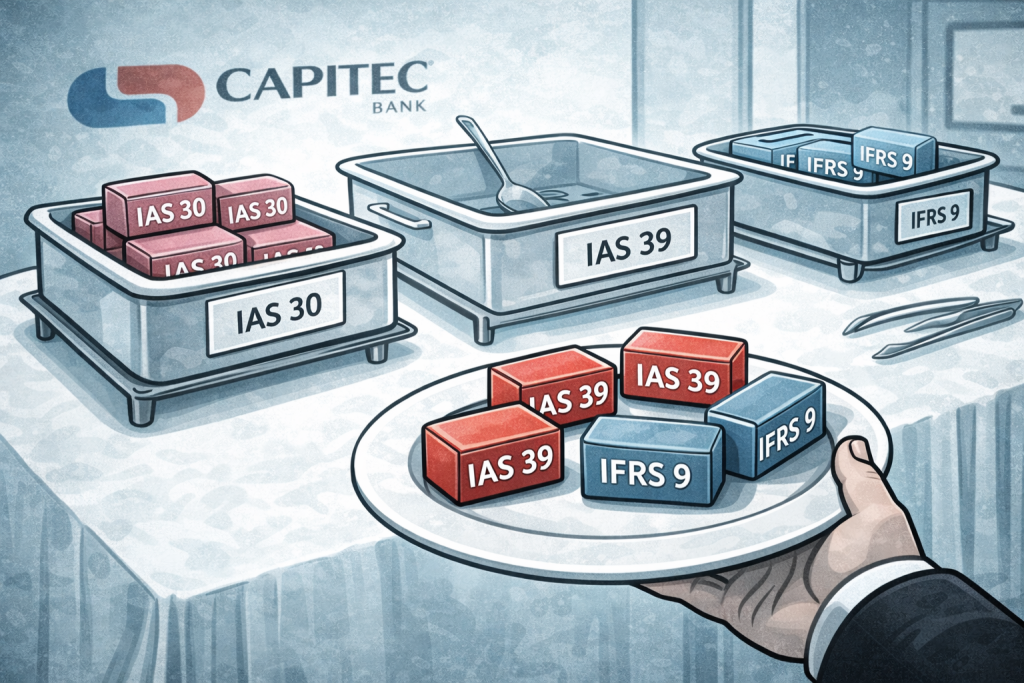

The crux of the tale lies in a technical shift from one accounting standard to another. IAS 39 would replace IAS 30 and introduce stricter rules around debt impairment and debt recoveries. Looming further down the road was IFRS 9, an even more stringent standard that Capitec cleverly continued to postpone adopting until it had no option but to adopt it in 2019. It’s not that Capitec couldn’t adapt to the new rules; it’s just that adopting them would end a little trick Du Plessis had up his sleeve. However, the auditors would need to be complicit to pull it off.

Here’s the trick: under IAS 30, Capitec wrote off any loans that were overdue for over three months. These loans vanished from the balance sheet, and any future recoveries were treated as delightful surprises — like finding a forgotten tenner in your coat pocket. However, the new accounting standards allowed for future recoveries, estimating how much might be clawed back from bad debts and reflected as a value today. You increase the gross loan balance and turnover by the estimated future recoveries. It’s a minor tweak, sure, but one with significant implications.

Du Plessis seized this opportunity like a magician pulling rabbits out of a hat. In 2009, Capitec added R11.3 million to its loan book, representing the present value of expected future recoveries. It doesn’t sound like much, but this sleight of hand boosted headline earnings by 5.4%. It was financial alchemy at its finest. Technically, there is nothing wrong with recognising recoveries before they materialise in IFRS 9. Save for the fact that you must also account for estimated future credit losses or bad debts to balance the scales. While deceptive, it wasn’t illegal, just as it wasn’t illegal for Lehman Brothers to exploit the loophole in FAS 140.

By the following year, the magic show was in full swing. Capitec doubled the trick, adding another R15.6 million in impairments to gross loans. Over a two-year period, the bank generated R38 million in “future recoveries,” impressing investors with what appeared to be higher profits and lower impairments. Du Plessis had expertly fiddled with the ratios analysts cared about most, making the numerator smaller and the denominator larger — the financial equivalent of wearing vertical stripes to appear slimmer. Capitec’s manoeuvre fell squarely into that “grey zone” where the rules were arguably open to interpretation but should have required meticulous disclosure and defensible assumptions.

Imagine if you could provide for future sales in your business — report them today, pat yourself on the back for record-breaking revenue, obtain your bonus, but hold off paying tax on those sales until they happen. A bit of accounting magic would make any entrepreneur’s eyes twinkle.

Critics might argue that Du Plessis didn’t overreach. After all, recoveries in 2009 were R46 million, climbing to R72 million in 2010 and reaching R100 million by 2011. But there’s more to that story — something we’ll dissect in a future chapter about how the multi-loan product worked and how they calculated recoveries. What’s more telling is how Capitec’s provisioning trends steadily declined, even as the loan book grew rapidly. On paper, it all looked marvellously optimistic.

Capitec’s executives had a polished narrative. They claimed their loan book quality improved thanks to better due diligence and tighter credit controls. Default rates were stabilising, and recoveries were climbing. Yet, how did the bank go from no recoveries in 2007 to R100 million by 2011?

In the world of finance, perception is reality. And while Capitec’s narrative was convincing, even the most minor cracks in that story could cast long shadows. By 2012, the fine print was starting to tell a more complicated tale that didn’t align with the bank’s straightforward, no-nonsense image. But, as with any good magician’s act, the audience often prefers the illusion to the truth.

- Capitec 2009 Annual Financial Statements pg. 20

- Capitec 2010 Annual Financial Statements pg. 95