An extract from ‘Boland Bankers Behaving Badly’, chapter 28. ‘Blockbuster’s Strategy’ from pages 139-145

In the summer of 2004, executives of a fledgling DVD-by-mail company called Netflix walked into the gleaming headquarters of Blockbuster Entertainment. They proposed that Blockbuster purchase Netflix for $50 million. The Blockbuster executives—titans of an empire spanning 9,000 stores across the globe—barely suppressed their laughter. Here was this upstart with his ridiculous red envelopes, suggesting he could replace the Friday night ritual of wandering the aisles of America’s favourite video store. They showed the Netflix execs the door. Today, Netflix is worth $386 billion. Blockbuster is a punchline.

Picture millions of South Africans, armed with what were once gold and are now black bank cards, standing patiently in the scorching African sun outside Capitec branches. ATMs from other banks sit empty and ignored just meters away. These customers have found their tribe. They’ve discovered something precious in a country where financial inclusion was a pipe dream: a bank that doesn’t make them feel poor for being poor.

Capitec claims 24.1 million clients in a country of 63 million people, of which only 7.4 million are taxpayers and 29 million are social grant recipients—four for every taxpayer. The official unemployment rate in South Africa is 32.9%, which means that most holders of Capitec bank cards are probably social grant recipients or people that we would technically call “unemployed.”

“What is interesting is when you look at the unemployment rate,” said Fourie in June 2025,” Stats SA doesn’t count self-employed people. I think that’s an area we need to correct. The unemployment rate is probably actually 10%. Just go look at the number of people in the township informal market, who are selling all sorts of stuff, who have a turnover of R1,000 a day.”

They’ve built this empire on radical simplicity: straightforward products, transparent pricing, and lower overall costs. The average Capitec Bank client pays just R48 a month in fees, compared to the Big Four’s average of R247. But here’s where the story takes a curious turn.

While their competitors have been quietly shuttering branches and pulling ATMs from street corners—embracing the digital future that seems as inevitable as sunrise—Capitec has been doing something almost incomprehensible. They’ve been building more branches and installing more ATMs. Many more.

By 2024, Capitec operated 42% more branches than any of the Big Four banks. While the industry’s ATM count plummeted 13% between 2019 and 2024, Capitec increased its count by a staggering 67%. They now run 75% more ATMs than FNB, South Africa’s largest bank. It’s the banking equivalent of opening more video stores in 2005. A poor strategy that’s well-executed doesn’t make it a good strategy; it makes it a well-executed poor strategy.

Fourie defends this counterintuitive strategy with arguments that would sound eerily familiar. Physical branches build trust, he insists. They foster personal connections. South Africans still need cash, still value face-to-face service. The branches and ATMs aren’t just convenient—they’re lifelines.

It’s the same logic that kept Blockbuster executives convinced that customers would always want to browse physical shelves, that the ritual of Friday night movie selection was irreplaceable, and that their stores offered something Netflix’s red envelopes could never match. They weren’t entirely wrong—until they were completely wrong.

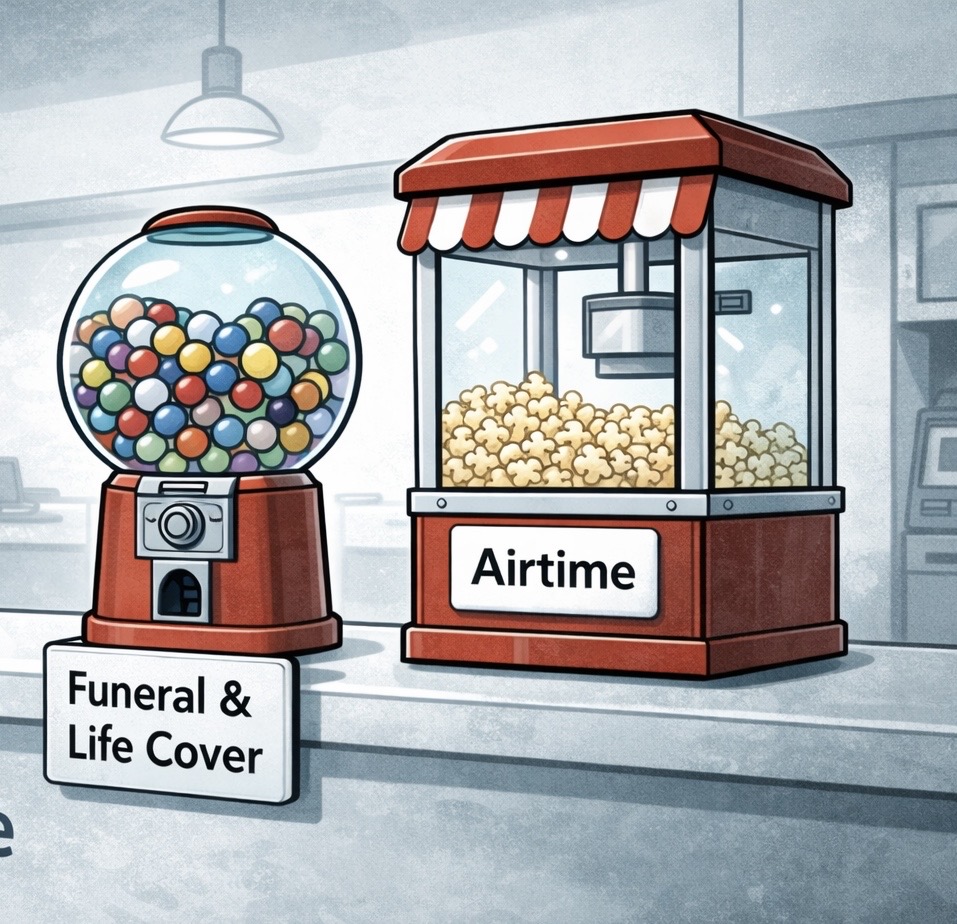

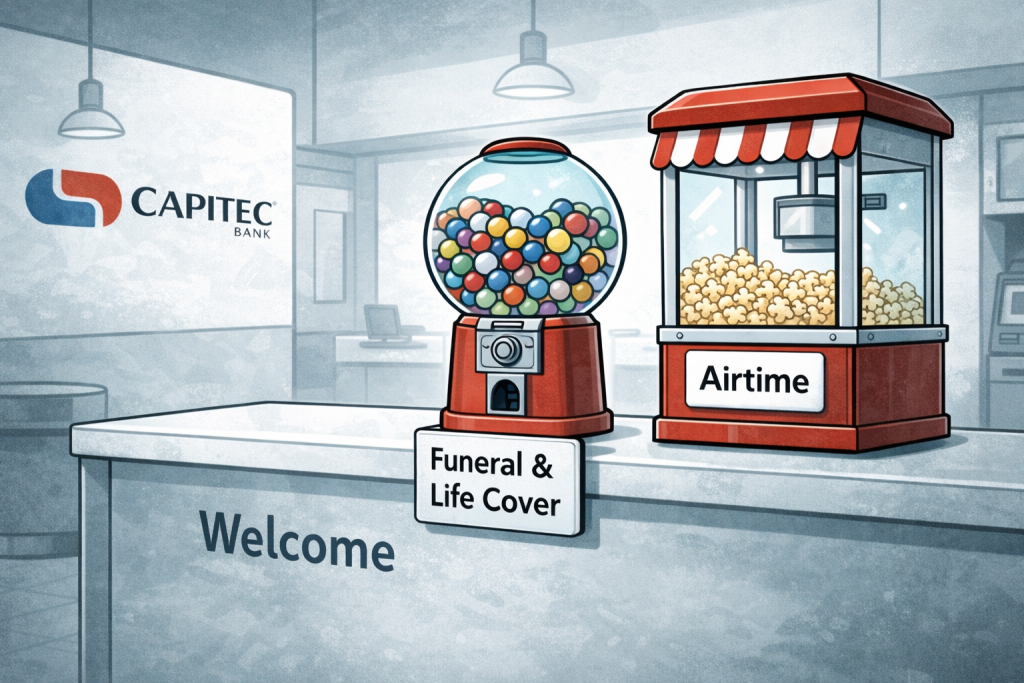

Peel back Capitec’s populist veneer, and you discover this isn’t a bank at all, at least not in the traditional sense. Like Blockbuster, which made its real money not from movie rentals but from late fees and concession sales, like popcorn, Capitec’s profits come from somewhere else entirely. Insurance sales. Cellphone top-ups. Electricity payments. The banking is almost beside the point.

Consider the mathematics of their operation. If Capitec truly has 25 million clients, but 11 million are “not fully banked”—generating only minimum fees—that’s roughly R1 billion in monthly revenue from customers who almost certainly cost more to serve than they contribute. It’s a loss-leader strategy that works brilliantly until it doesn’t. Considering the number of active bank accounts claimed by all banks, the total exceeds 86 million. In a population of 63 million, this means that people operate more than one “primary” bank account.

The rest of the chapter can be found here.

Note: The original book includes footnotes and references. To read the rest of the chapter, subscribe to my Substack.